Diminished Value Claim: Recover Value Post-Accident

A car accident in the United States often happens when you least expect it. No matter how defensively I drive, I cannot always avoid the car rear-ending me at a red light. While the primary concern in an accident is physical injury, the harsh reality is that the sudden evaporation of your valuable asset’s worth brings an enormous amount of stress.

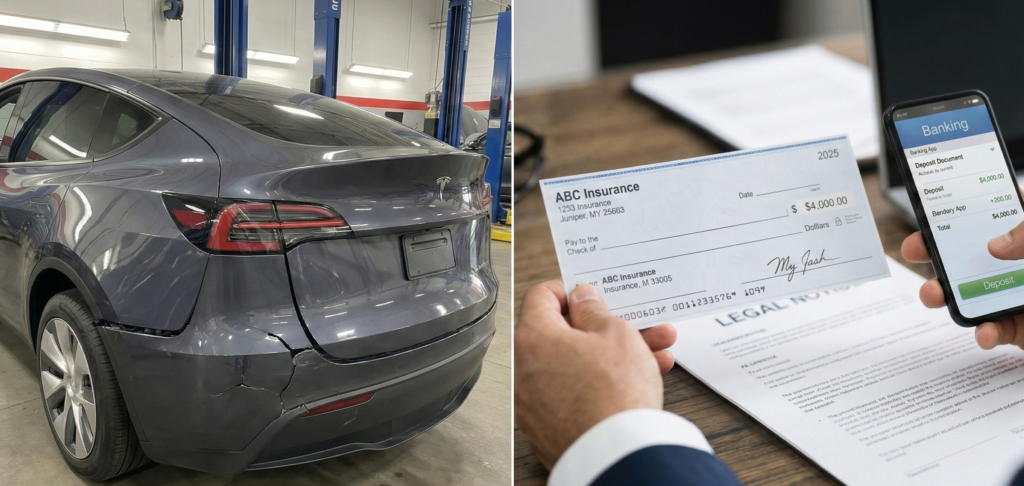

I recently experienced an incredibly frustrating incident. I had just purchased a brand new 2025 Tesla Model Y Juniper, and it was involved in an accident exactly two weeks after delivery. It was fully loaded with the Full Self-Driving (FSD) option, making the vehicle’s total cost nearly $60,000. It was completely spotless until that moment.

Because the other driver was 100% at fault, their insurance naturally covered the repair costs. However, the moment my car was fixed and a single line reading ‘Accident Reported’ appeared on the CarFax report, my vehicle was no longer a new car. It felt incredibly unfair. That is why I decided to fight the insurance company, and ultimately, I managed to secure an additional $4,000 in compensation on top of the repair costs.

Today, I will share my practical, firsthand experience and explain exactly what a Diminished Value Claim is. More importantly, I will share the negotiation strategy I used to get a fair payout from the insurance company without having to pay for an expensive, certified appraisal report upfront.

📘 1. The Hidden Cost of US Car Accidents: What is Diminished Value?

If you drive in the United States, Diminished Value is a concept you absolutely must understand. Simply put, it is the reduction in your vehicle’s resale market price solely because it now has an accident history.

📉 Why Does the Value Drop So Much? (Inherent DV)

Let us say you get into an accident, replace the bumper, fix the fender, and get a flawless paint job. On the outside, the car looks exactly like a brand new one. However, the logic of the used car market is incredibly cold and objective.

- The Stain on the Record: Dealers and private buyers will always check CarFax or AutoCheck reports before making an offer.

- Psychological Factors: Buyers naturally worry about structural damage or latent defects, causing them to significantly lowball the price compared to an identical accident-free car.

- The Result: Regardless of how perfectly the car was repaired, the sheer existence of the accident history causes a persistent drop in value. This is known as Inherent Diminished Value, and this is exactly the money we need to claim.

⚙️ 2. The Insurance Company’s Defense Logic: The Trap of the 17c Formula

The moment I filed my Diminished Value Claim with the insurance company, they immediately pulled out their favorite tool: the 17c Formula. This calculation method originated from a court case in Georgia, and insurance companies wield it like a shield to minimize their compensation payouts nationwide.

🚫 Why the 17c Formula is Terrible for High-End Car Owners

This formula is completely inadequate for high-value new cars, especially those packed with advanced technology sensors and battery packs.

- The 10% Cap: The formula limits the maximum Diminished Value payout to just 10% of the car’s pre-accident value. For my vehicle, their logic dictates that no matter how severely it was damaged, they will never pay more than the artificially capped limit.

- Double Mileage Deduction: When calculating the pre-accident value, the car’s mileage is already factored in. However, the formula maliciously applies another mileage multiplier at the very end, effectively penalizing you twice.

- Lack of Market Reality: Electric vehicles like Tesla suffer a much steeper depreciation curve after an accident due to buyer fears regarding potential battery or sensor damage. The 10% rule completely ignores this harsh reality of the current EV market.

🥊 3. [Real Case Study] How I Won Compensation for My 2-Week-Old Tesla

My situation was quite special. I had a two-week-old 2025 Model Y Juniper with less than 500 miles on the odometer. Anyone looking at the market knows this is the exact sweet spot where depreciation hits the hardest.

📝 Step 1: The Initial Demand Claim

I utilized AI tools like ChatGPT and Gemini to calculate my car’s current market value and the estimated depreciation caused by the accident. Combining this data with advice from a local attorney, I concluded that I needed to receive a significant amount. I sent a formal email to the insurance adjuster immediately.

“My vehicle is a two-week-old new car. My market research indicates a minimum 15% drop in value due to the accident history. I am officially demanding diminished value compensation.”

🗣️ Step 2: The Insurance Company’s Counter Demand for Proof

The insurance company responded exactly as I expected them to. They requested an official Appraisal Report from a Licensed Appraiser, along with a written statement from the repair shop, as objective supplementary documents. They stated that until then, they would not pay a single cent.

This put me in a difficult dilemma. Getting a professional appraisal report usually costs between $400 and $500 out of pocket. I had to weigh whether it was worth spending the money upfront just to chase a claim, especially since the insurance company might still refuse to pay.

⚖️ Step 3: The Lawyer’s Brilliant Leverage

At this point, the lawyer handling my accident gave me some incredibly brilliant advice. He told me there was no need to spend money on a report. Instead, we used time and certainty as our primary negotiation weapons.

Our negotiation logic was simple but effective. We argued that an appraisal would easily show a massive loss because this is a brand new car, potentially leading to a lawsuit. We pressured them by highlighting the costs of litigation. Finally, we offered a clean settlement right now without any appraisal reports.

🏆 Step 4: The Final Settlement Victory

A few days later, the insurance company finally waved the white flag. By skipping the appraisal fee and the stressful procedures, we reached a final settlement. While it was slightly less than my initial target, saving the appraisal cost and time meant I practically achieved my real goal.

📝 4. The 4-Step Guide to Claiming Diminished Value in the US

Based on my personal battle, I have organized a streamlined 4-step process to help you secure a fair Diminished Value payout if you are ever involved in an accident in the US.

① Check Your Eligibility

Not every accident qualifies for a Diminished Value claim.

- 100% Not at Fault: If you share any blame for the accident, filing a claim becomes extremely difficult, except in specific states like Georgia.

- Vehicle Age and Mileage: Your chances of winning are much higher if your car is less than five years old and has under 100,000 miles.

- Repair Cost Scale: Larger accidents with repair bills exceeding $3,000 make for a much stronger and more profitable case.

② Gather Evidence and Run Calculations

You cannot just demand money blindly; you need solid logic to back it up.

- Use AI: Prompt an AI by stating the make, model, mileage, and repair costs to get a realistic baseline.

- Compare Online Quotes: Get instant online offers from CarMax or Carvana. Enter your car’s details once claiming “no accidents,” and a second time with the “accident history.” The difference between these two offers is your absolute best proof of loss.

③ Send the Official Demand Letter

Send a formal email to the insurance adjuster. Keep your message concise, logical, and firm rather than emotional.

“I do not accept the 17c formula. I am demanding compensation for the Actual Cash Value Loss of my vehicle. Based on market research, my vehicle has suffered significant diminished value.”

④ Master the Negotiation Phase

The insurance company will always reject your first offer or lowball you immediately. You have two main options here.

- Option A (With a Lawyer): If you have an attorney, let them handle it. They know exactly how insurance companies operate and can use the promise of a “quick settlement” as powerful leverage.

- Option B (Handling it Yourself): If you do not have a lawyer, it is actually better to spend the money on a professional DV Appraisal Report. A document stamped by a licensed expert carries much more weight.

⚠️ 5. Critical Warning: Before You Sign the Release Document

When you finally reach a settlement figure you agree on, the insurance company will force you to sign a document called a “Release of Property Damage Claim” before they wire the funds. This document is a legal contract stating that in exchange for the money, you will never pursue them for vehicle damages related to this specific accident again.

🛑 Timing the Signature

Never rush this step. Take your repaired car back, drive it for a few days, and ensure there are no weird rattling noises or peeling paint before you sign away your rights. You must be absolutely certain the repairs were done correctly.

🔍 Verify the Scope

Read carefully to ensure the release applies strictly to “Property” damage only. If the document sneakily mentions “Bodily Injury,” absolutely do not sign it, because physical pain from an accident can surface weeks or months later. Insurance companies often try to bundle these claims together to minimize future liability.

✅ 6. Conclusion: The Law Does Not Protect Those Who Sleep on Their Rights

Insurance companies in the United States are highly profitable, for-profit corporations. They are absolutely not on your side. If you do not explicitly demand your Diminished Value, they will never voluntarily offer you a single penny for it.

In my scenario, the unique condition of having a two-week-old new car, combined with my lawyer’s sharp negotiation skills, allowed me to get a great result without paying for an appraisal report. However, in most standard claims, investing in an expert’s report might be necessary. The most critical lesson here is that you simply must not give up.

Getting your fair share might seem like a small victory to some, but for an owner who unfairly had their new car wrecked, it was the minimum financial therapy I needed to move on. If you ever get into a car accident in the US, do not just accept the repair costs and walk away. You must fight for every single dollar of your vehicle’s lost value.

🔗 External Links

- National Association of Insurance Commissioners: State Insurance Consumer Guides https://content.naic.org/consumer/home

- Insurance Information Institute: The Basic Concepts of Diminished Value https://www.iii.org/article/what-is-diminished-value

- Kelley Blue Book (KBB): Check Your Car’s Pre-Accident Value https://www.kbb.com/

- Edmunds: How to File a Diminished Value Claim https://www.edmunds.com/car-insurance/how-to-file-a-diminished-value-claim.html